Who Needs an LEI in Canada? Common Triggers for Registration

Many Canadian organisations only learn about LEIs when a bank, broker, trade repository, or compliance team asks for one at short notice. That can make the requirement feel narrow or highly technical. In practice, the trigger is often much simpler: if a legal entity is involved in certain regulated financial activity, especially reportable OTC derivatives activity, an LEI may be required and it must stay active.

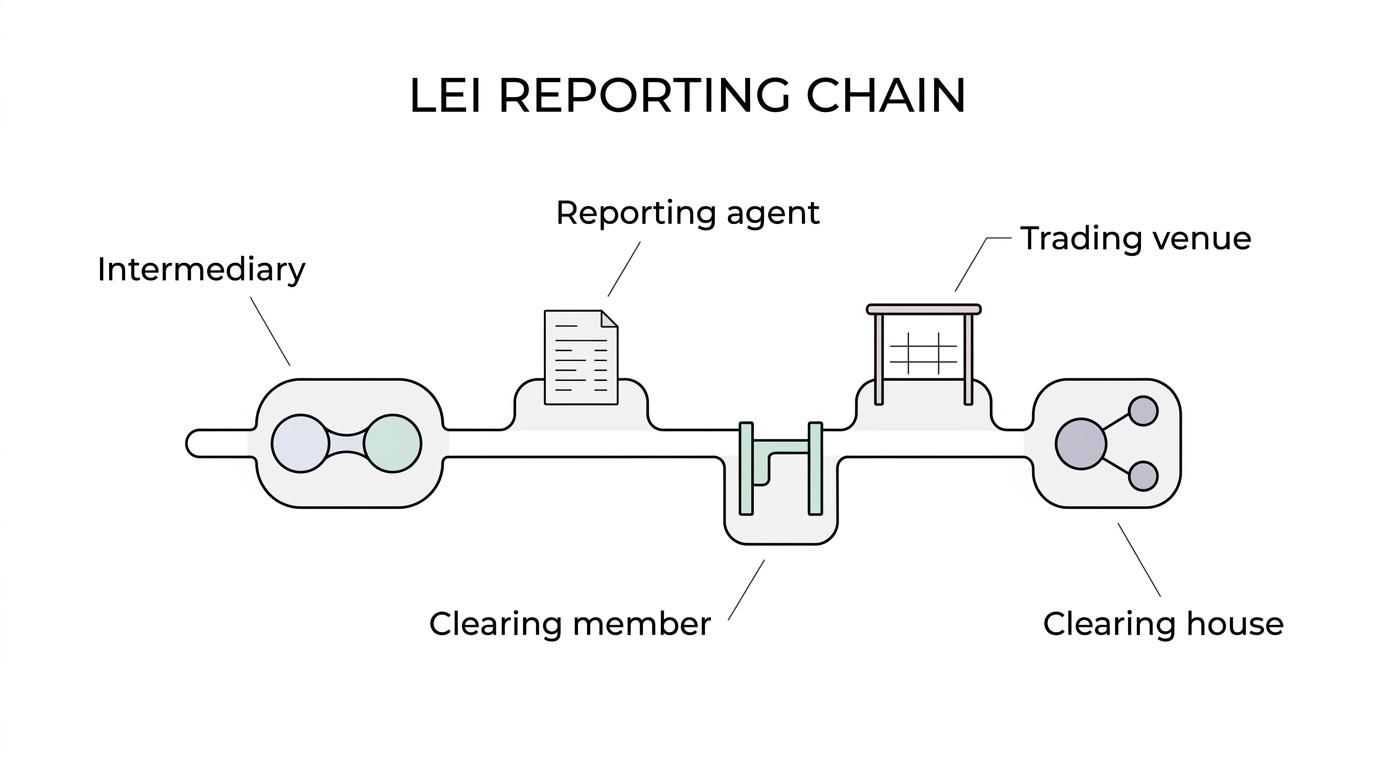

The key point is that an LEI in Canada is not only for the obvious trading party. Securities guidance has made that clear. Depending on the role an entity plays in a transaction or reporting chain, the requirement can extend to intermediaries, reporting agents, clearing participants, trading venues, and clearing houses as well.

What an LEI is for Canadian legal entities

A Legal Entity Identifier, or LEI, is a unique 20 character alphanumeric code assigned to a legal entity. The global LEI system is based on ISO 17442 and is administered by the Global Legal Entity Identifier Foundation, or GLEIF. Each LEI links to verified reference data drawn from authoritative local sources, including core organisational details and, where available, ownership information.

That matters because the LEI is not just an internal number used by regulators behind the scenes. LEI records are published in the Global LEI Index, which is open and free to access. Regulators, data providers, counterparties, and legal entities themselves use that public record to confirm who is participating in financial transactions.

An LEI is therefore best seen as a standard identity credential for legal entities in financial markets.

Which Canadian entities often need an LEI

Not every corporation, charity, fund, or partnership in Canada needs an LEI by default.

What matters is the activity and the role. If an entity enters into reportable OTC derivative transactions, participates in the reporting process, or sits inside the market infrastructure connected to those trades, the LEI requirement can apply. Individuals do not receive LEIs. Legal entities do.

The range is wider than many teams expect:

- corporations

- investment funds

- pension arrangements

- trusts and partnerships

- charities with relevant market activity

- intermediaries and market infrastructure entities

A quick way to think about it is this: if the entity must be identified in a regulated derivatives record, there is a strong chance an LEI is part of the requirement.

| Entity type or role | Common LEI trigger in Canada | Practical note |

|---|---|---|

| Company or corporate group entity | Entering into reportable OTC derivatives | The LEI identifies the legal entity, not the trading desk |

| Investment fund | OTC derivatives reporting or related compliance obligations | Funds often need an LEI even when a manager handles operations |

| Charity or non-profit legal entity | Financial market activity that falls within reporting rules | Legal form does not remove the requirement |

| Broker acting as intermediary | Role connected to a reportable trade | Ontario guidance names this role directly |

| Reporting agent | Submitting or managing trade reporting | A non-trader can still need its own LEI |

| Clearing member | Participation in clearing for a reportable transaction | LEI supports consistent entity identification |

| Electronic trading venue | Venue linked to reportable OTC derivatives activity | Covered in Ontario guidance |

| Clearing house | Infrastructure role tied to reportable trades | Also identified in Ontario guidance |

OTC derivatives reporting is a major LEI trigger in Canada

For many entities, the main Canadian trigger is OTC derivatives reporting. Canadian Securities Administrators announced final amendments to derivatives data reporting standards on July 25, 2024, with the changes taking effect on July 25, 2025. Alongside that update, market participants transacting OTC derivatives were reminded that they must renew their LEI.

That reminder carries real compliance weight. The CSA stated that a Canadian market participant with outstanding OTC derivatives that does not renew its LEI is not in compliance with securities law. So the issue is not only getting an LEI once. A lapsed LEI can create a compliance problem where trades remain outstanding.

This is where many entities get caught out. They registered an LEI years ago, used it for onboarding or reporting, and then let the annual renewal pass. When reporting standards tighten or counterparties refresh their controls, the lapse becomes visible very quickly.

A few common situations tend to trigger urgent LEI checks:

- new OTC derivatives activity

- outstanding trades with a lapsed LEI

- onboarding by a broker or dealer

- reporting remediation before a filing deadline

- cross-border trading relationships

Ontario LEI guidance includes non-trader roles

Ontario guidance is especially useful because it makes the scope more concrete. Under OSC Rule 91-507, all companies that offer reportable OTC derivative transactions must have an LEI. The guidance also names several roles that are easy to overlook if the business does not think of itself as the trader.

Those roles show why the question “Do we trade?” is sometimes too narrow. The better question is “Are we identified anywhere in the lifecycle, reporting flow, or infrastructure of a reportable OTC derivative?”

Ontario guidance identifies these roles directly:

- Reporting agent: an entity submitting or managing reporting tied to the transaction

- Broker acting as an intermediary: a broker involved between parties to a reportable trade

- Clearing member: an entity participating in the clearing chain for the transaction

- Electronic trading venue: a venue connected to the execution of a reportable trade

- Clearing house: an organisation supporting central clearing linked to the reported transaction

That broadens the practical answer to who needs an LEI in Canada. The requirement can attach to participation in the market structure around the trade, not only to the named counterparty.

Funds, charities, and private companies can all fall within LEI requirements

The legal form of the entity is not the deciding factor. A private company may need an LEI while another company in the same industry does not. A charity may need one if it enters into reportable transactions or appears in reporting through a relevant role. A fund may need one even where the manager or adviser runs most external operations.

The question is functional. Is the legal entity engaged in activity that brings it into a regulated reporting framework? If yes, an LEI can become necessary very quickly.

This also explains why many entities are first asked for an LEI by a third party. A dealer, trade repository, bank, custodian, or service provider may be checking whether the entity can be properly identified in the reporting chain. By the time that request arrives, the LEI is often no longer optional from a practical standpoint.

One legal entity should have one LEI

The LEI system is built around uniqueness. Ontario guidance states that each entity may receive only one LEI and that the same identifier must be used for all LEI reporting in each jurisdiction where it is required.

That single-identifier rule reduces confusion across systems and regulators. It also means an entity should avoid applying again if it already has an LEI, even if the status has lapsed or the original registration was completed through another provider. In that situation, the right step is usually renewal or transfer and renewal, not a second application.

A reliable registration process should include a registry and GLEIF lookup before submission so duplicate LEIs are avoided.

LEI renewal in Canada matters just as much as registration

An active LEI is generally renewed every year. The annual renewal is not just an administrative preference. It confirms that the reference data linked to the entity is still current and that the LEI remains in good standing.

Because the LEI record is public, counterparties and regulators can see whether it is active or lapsed. If the entity is involved in reportable OTC derivatives and the LEI has not been renewed, that status can interrupt onboarding, reporting, or internal compliance sign-off.

A strong renewal process usually includes three things:

- Calendar control: annual reminders well ahead of expiry

- Reference data review: legal name, address, registration details, and ownership information checked against current records

- Ongoing maintenance: updates submitted when core entity data changes, not only at renewal time

Multi-year management can help here, especially for groups or funds handling several LEIs at once. It reduces the risk of expiry slipping past during busy reporting periods.

How Canadian entities can register an LEI without delays

The registration itself is usually straightforward when the entity details are ready and the application is checked against official records. The challenge is often timing. Teams tend to start the process only after a trade, onboarding file, or reporting task is already in motion.

That is why speed, duplicate checks, and support matter. A registration agent can help legal entities obtain, renew, or transfer an LEI while checking the registry and the Global LEI Index to avoid accidental duplicate applications. For organisations managing multiple entities, bulk arrangements and centralised renewals can make administration much cleaner.

Some providers also offer practical service features that reduce friction for Canadian applicants:

- Fast issuance: same-day processing may be available for orders placed before a stated morning cut-off

- Express option: urgent applications can sometimes be handled within two hours

- Support access: phone and unlimited email support can help when legal form, documentation, or status questions come up

- Free data updates: reference data maintenance may be included so core details stay current with GLEIF records

Price matters too, though it should be judged alongside service and renewal support. Some providers offer multi-year pricing from C$69 per year with GLEIF fees included, while single-year and longer-term pricing can vary by provider and service level. If the entity expects to remain active in regulated markets, a multi-year option often gives both cost certainty and better renewal discipline.

A practical test for whether an LEI is needed in Canada

If a legal entity in Canada is entering into reportable OTC derivatives, appears in the reporting chain, or serves as part of the related market infrastructure, the safest assumption is that an LEI may be required. That includes entities that do not see themselves as traditional traders.

A quick internal check can help compliance teams move faster:

- Is the party a legal entity rather than an individual?

- Is it involved in reportable OTC derivative transactions?

- Is it named in reporting, intermediation, clearing, or venue activity tied to those transactions?

- Does it already have an LEI that may need renewal rather than replacement?

When those answers point toward the LEI system, acting early is the better path. It keeps onboarding cleaner, reporting more reliable, and compliance teams away from avoidable last-minute work.