LEI for OTC Reporting in Canada

For many Canadian entities, OTC derivatives reporting has turned the LEI from a back-office detail into an active compliance item. If your business, fund, charity, or other legal entity is party to a reportable derivative, the status of your Legal Entity Identifier can now affect whether you are meeting securities law obligations.

That shift matters even if your organisation is not the reporting counterparty. Canadian rules tie LEI maintenance to the life of open reportable derivatives, which means renewal is not optional while those positions remain outstanding.

Why OTC reporting LEI rules in Canada matter in 2025

Canadian securities regulators announced final amendments to OTC derivatives data reporting standards on July 25, 2024, with the changes taking effect on July 25, 2025. One of the clearest messages from that rollout is that entities with outstanding OTC derivatives cannot treat an LEI as a one-time setup task.

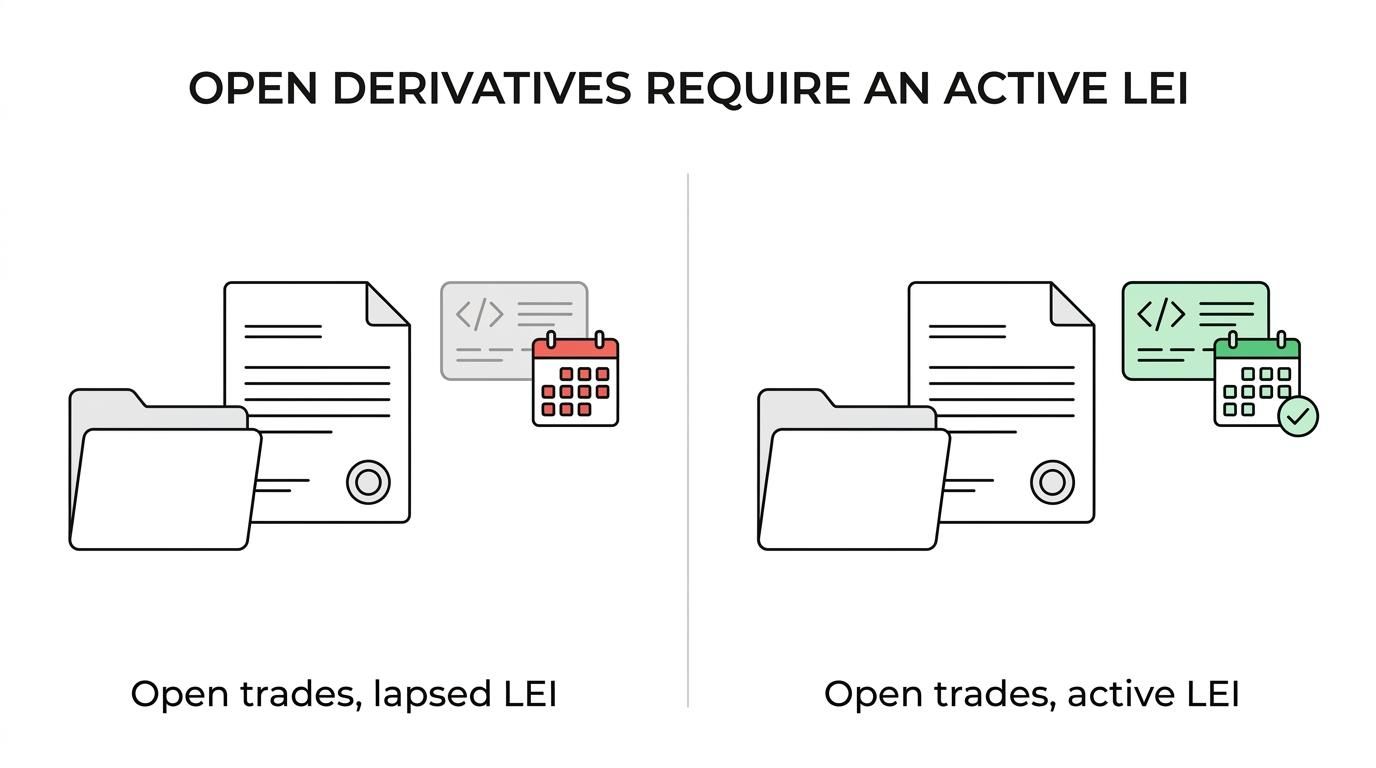

The Canadian Securities Administrators stated that any Canadian market participant with outstanding OTC derivatives that does not renew its LEI is not in compliance with securities law. That is a direct compliance signal, not a soft recommendation.

For legal entities active in swaps, forwards, options, or other reportable derivatives, this creates a simple operational rule: if the trade remains reportable and open, the LEI must remain active as well.

What an LEI means for OTC reporting in Canada

An LEI is a unique 20-character alphanumeric code issued through the Global LEI System. GLEIF, the Global Legal Entity Identifier Foundation, states that the code is based on ISO 17442, identifies one legal entity only, and connects that entity to verified reference information.

That may sound technical, yet the purpose is straightforward. Regulators, trade repositories, counterparties, and market infrastructure need a reliable way to identify legal entities across transactions and reporting records. When the LEI is current, the reporting chain is cleaner and easier to validate.

After that basic definition, a few features stand out:

- 20-character global identifier

- One LEI for one legal entity

- Verified reference data

- Annual renewal cycle

When Canadian local counterparties must obtain and renew an LEI

The current Canadian framework is broader than many firms expect. Under the Ontario guidance issued with the trade reporting amendments, a local counterparty other than an individual that is party to a reportable derivative must obtain, maintain, and renew an LEI whether or not it is the reporting counterparty.

That means a non-reporting counterparty cannot assume the dealer, clearing participant, or another reporting entity has “covered” the issue. The rule attaches to the entity’s status as a local counterparty to a reportable derivative.

The timing piece is just as clear. The obligation continues for as long as the counterparty has open derivatives that are required to be reported. Once all reportable derivatives have expired or terminated, the entity is no longer required to maintain or renew its LEI until it enters into a new derivative.

The table below captures the practical effect.

| Situation | LEI expectation in Canada |

|---|---|

| Local counterparty enters a reportable derivative | Must obtain an LEI if it does not already have one |

| Local counterparty is not the reporting counterparty | Still must maintain and renew the LEI |

| Open reportable derivatives remain outstanding | LEI must stay active through renewal |

| All reportable derivatives have expired or terminated | Renewal obligation stops until a new reportable derivative is entered |

| LEI lapses while open reportable derivatives remain | Compliance risk under securities law |

Open derivatives, expired contracts, and lapsed LEI risk

This distinction between open derivatives and fully expired or terminated contracts is where many compliance teams need sharper internal controls. An entity may think of LEI renewal as an annual registry task, while the rule treats it as position-dependent. If trades remain open, the LEI has to remain current.

A lapsed LEI is not just an administrative blemish. In the OTC reporting setting, it can create data quality issues, delays in reporting workflows, and direct regulatory exposure. It can also trigger avoidable follow-up with counterparties, legal, operations, and compliance teams trying to fix a gap after the renewal date has passed.

The main risk points are easy to summarise:

- Open position: renewal remains required

- Expired or terminated portfolio: renewal may no longer be required

- Lapsed LEI with outstanding OTC derivatives: potential non-compliance

- Late internal review: greater chance of missed reporting deadlines

Practical OTC reporting LEI steps for Canadian entities

A workable compliance process starts with one question: do we currently have any open reportable derivatives? That question should sit with treasury, legal, operations, and compliance together, because the answer often lives across more than one system.

The next step is matching position status to LEI status. If your entity has open reportable derivatives, the LEI should be valid and renewed on time. If the LEI is close to expiry, renewal should happen before the lapse date, not after a counterparty or repository flags the issue.

A strong internal process often includes the following sequence:

- Identify positions: confirm whether any reportable OTC derivatives remain open.

- Check LEI status: verify that the legal entity’s LEI is active and not nearing lapse.

- Assign ownership: make one team or role responsible for renewal monitoring.

- Review after terminations: once all reportable derivatives end, reassess whether renewal is still required.

This is especially useful for groups with multiple entities. One affiliate may still have open derivatives while another has fully exited reportable activity. Treating the entire group the same can lead either to unnecessary renewals or, worse, missed renewals where the obligation still exists.

OTC reporting LEI governance for funds, corporates, and charities

The Canadian rule set reaches across a wide range of legal entities. Public companies are not the only ones that need to pay attention. Investment funds, special purpose vehicles, charities, pension-related entities, and private corporates may all find themselves within the reporting framework when they enter reportable derivatives.

That broad scope is why governance matters. The LEI should sit on the same checklist as reporting status, trade repository fields, counterparty onboarding data, and regulatory change monitoring. When those tasks are split too widely, renewal is easy to overlook.

A practical governance model often includes a few simple controls:

- renewal calendar with reminders

- named internal owner

- quarterly check of open derivatives

- documented policy for when renewal can stop

LEI renewal timing and data accuracy for Canadian reporting

Renewal is not only about paying a fee and keeping a code active. The LEI record also links to reference data about the legal entity, and that data should remain current. If an entity changes its legal name, registered address, or other core details, those updates should be reflected properly.

That matters in OTC reporting because regulators and market participants rely on the LEI as part of a standardised identity framework. Accurate reference data supports cleaner matching, fewer manual interventions, and stronger confidence in the reported record.

For firms managing multiple deadlines, this creates a useful discipline: pair LEI renewal reviews with entity data checks. One review cycle can cover both the renewal date and any needed updates to the underlying reference information.

Choosing an LEI registration and renewal process in Canada

Speed and reliability matter when a trade is pending or a renewal date is close. A provider should be able to help with new registration, renewal, and transfer, while checking existing registry records to reduce the chance of duplicate applications.

For Canadian entities dealing with OTC reporting timelines, support quality also matters. Questions often come up around whether a derivative is still open, whether an entity qualifies as a local counterparty, or whether a lapsed LEI can be restored quickly enough to limit disruption. Clear phone and email support can save time when internal teams need answers fast.

LEI Service focuses on this type of process support. Its offering includes new LEI registration, renewals, transfers, multi-year management, free data updates, and English-speaking phone and email support. Issuance can be same day if ordered before 11 AM, with an express option within two hours, which can be helpful when reporting or onboarding timelines tighten.

Pricing can also shape the decision, especially for entities managing several affiliates or fund structures. Multi-year plans from C$69 per year with GLEIF fees included, plus bulk arrangements for larger volumes, can make ongoing administration simpler and more predictable.

How Canadian entities can avoid last-minute OTC reporting LEI issues

The easiest problems to fix are the ones caught early. A quick monthly or quarterly check of open reportable derivatives against LEI renewal dates can prevent a year-end scramble or a failed onboarding process.

This is one area where small operational habits produce outsized value. Keep a current list of legal entities, note which ones are local counterparties, record whether they have outstanding OTC derivatives, and track renewal dates in one place. If all reportable derivatives for an entity have expired or terminated, document that status clearly so the business knows why renewal was paused.

When new derivatives activity starts again, the LEI question should return at the very beginning of the workflow, right beside legal entity verification and reporting setup. That keeps the rule where it belongs: not as an afterthought, but as part of the normal discipline of OTC derivatives reporting in Canada.