LEI for Investment Funds: Common Scenarios and Setup Tips

An investment fund can be fully formed, properly documented, and ready to launch, yet still hit an operational stop because one key identifier is missing. That identifier is often the Legal Entity Identifier, or LEI.

For fund managers, trustees, general partners, and administrators in Canada, the LEI is rarely just a box-ticking exercise. It can affect trading access, derivatives reporting, counterparty onboarding, and the speed of a fund launch. When the timing is tight, getting the setup right early matters.

Why an investment fund may need an LEI

An LEI is a global identifier for legal entities involved in financial transactions. For investment funds, the main question is not whether LEIs exist, but which entity in the structure needs one and when.

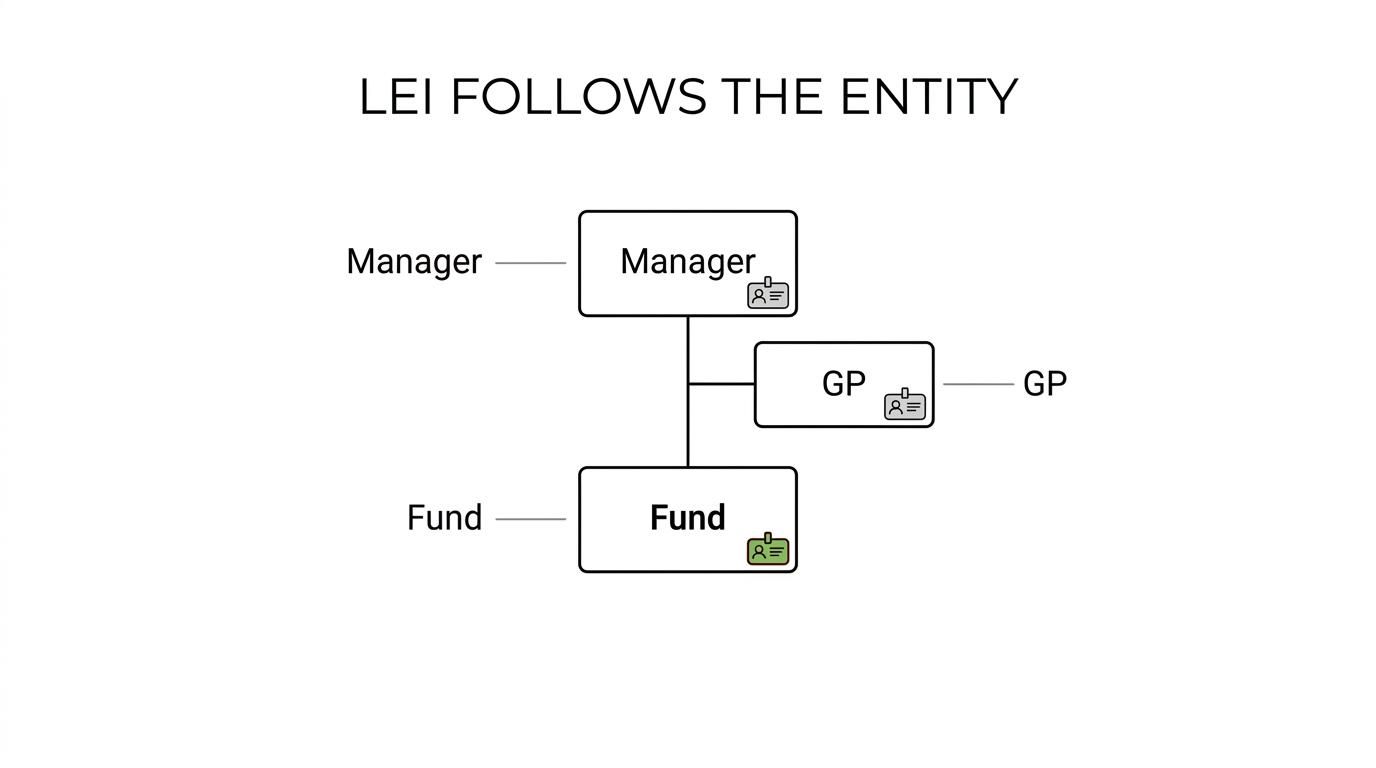

That distinction matters because a fund complex may include several separate legal vehicles. A manager may have its own LEI. The general partner may have another. The fund itself may need its own LEI as well. In a master-feeder structure, more than one fund vehicle may need to be identified independently.

A good rule is simple: if the fund itself is the legal counterparty, the reporting entity, or the entity being onboarded by a broker or custodian, the fund usually needs its own LEI.

Funds that commonly run into LEI requirements include:

- Hedge funds

- Private equity funds

- Venture capital funds

- Mutual funds

- Exchange-traded funds

- Commodity pools

- Master and feeder funds

- Parallel funds

- Umbrella funds and sub-funds

Common LEI scenarios for investment funds

Many funds do not apply for an LEI on formation day. The trigger usually comes when the fund starts interacting with market infrastructure, counterparties, or regulators.

In practice, a few scenarios show up again and again.

| Scenario | Why the LEI matters | Typical impact |

|---|---|---|

| Trading with an EU or UK investment firm | Transaction reporting frameworks often require a legal entity identifier | Trading may be delayed until the LEI is active |

| Entering derivatives | Trade reporting under EU, UK, and some Canadian rules uses LEIs | The fund may need an LEI before reporting can be completed properly |

| Filing private fund reports | Some U.S. filings request the fund LEI if applicable | Advisers may need it to keep filings complete and consistent |

| Opening prime brokerage or custody accounts | Counterparties often ask for LEIs during onboarding | Account opening can slow down without one |

| Securities lending or repo activity | Reporting regimes for securities financing transactions identify legal entities by LEI | Operational readiness depends on current LEI data |

| Fund restructuring or name change | LEI reference data must stay current | A lapsed or outdated record can create compliance friction |

The strongest mandatory patterns appear in Europe and the UK, especially where transaction reporting or derivatives reporting is in scope. Canada can also bring LEIs into the picture through derivatives trade reporting, depending on the structure and activity involved.

The U.S. can feel less absolute, yet the LEI still becomes relevant in reporting and institutional workflows. That is why many Canadian funds with cross-border activity choose to arrange their LEI well before the first trade rather than wait for a counterparty to ask.

LEI setup tips for investment fund structures

The most common LEI mistake is applying for the wrong entity.

That sounds basic, but it happens often in structures with advisers, trustees, GPs, managers, sub-funds, and special purpose vehicles. A fund may assume the management company’s LEI is enough, only to learn that the actual trading counterparty is the fund itself.

Before starting an application, it helps to map the structure on one page and identify who will actually appear in onboarding records, reporting systems, and trade documentation.

A practical setup review should cover a few points:

- Entity scope: confirm whether the LEI is needed for the fund, the GP, the manager, the trustee, or multiple vehicles

- Use case: identify whether the driver is trading, derivatives reporting, securities financing, custody onboarding, or regulatory filing

- Fund structure: check whether master-feeder, umbrella, parallel, or sub-fund arrangements create separate LEI needs

- Jurisdiction: match the application data to the registry or formation authority that governs the fund entity

- Applicant authority: make sure the person filing has authority to act for the fund

- Timing: allow for validation time, not just form submission time

For newly launched funds, timing is often underestimated. A simple application can move quickly, but validation still depends on official source data and the complexity of the structure. If the fund is offshore, newly formed, trust-based, or not easily visible in a registry, more follow-up may be needed.

That is why a launch checklist should include LEI timing just as early as bank account opening, tax registrations, and subscription document review.

Getting the application data right

LEI records are only as good as the reference data behind them. For funds, that means the legal name, registered address, registration number, legal form, and formation jurisdiction should match official records exactly.

Even small mismatches can slow approval. Abbreviations, punctuation, and address formatting may look minor internally but can trigger validation questions.

A short internal fact sheet can save a surprising amount of time. It should pull the fund’s exact legal details from formation documents, registry extracts, and existing compliance records so everyone uses the same source data.

Documents and details an investment fund should prepare

The required package varies by issuer and by the fund structure, though the pattern is consistent. Straightforward corporate entities tend to move faster. Partnerships, trusts, umbrella structures, and recently formed vehicles may need extra support.

Most funds should be ready to provide:

- Legal name and registered address

- Formation or incorporation number

- Jurisdiction of formation

- Registration authority details

- Legal form

- Contact details for the applicant

- Evidence of authority to apply on behalf of the fund

If the structure is more complex, additional records may be useful. A limited partnership agreement extract, trust deed excerpt, offering memorandum, registry extract, or organization chart can help validate the entity more efficiently.

One practical tip stands out: use the same naming and entity descriptions that appear in your fund documents and onboarding files. If your administrator, counsel, and onboarding team all describe the entity differently, delays become much more likely.

Choosing an LEI provider for a fund application

Not all LEI workflows feel the same, even though the end result should be a valid LEI published through the global system.

For funds, the first check is straightforward. The LEI must be issued through a GLEIF-accredited issuer, or through a registration agent working with one. That is the baseline. After that, service quality starts to matter.

A provider that handles standard corporations well may still struggle with fund-specific questions. That is why it helps to ask whether the underlying issuer can process fund entities and whether the service team is comfortable with partnerships, trusts, and multi-entity fund structures.

When comparing providers, it is worth looking at:

- Fund capability: can the provider handle investment funds rather than only ordinary operating companies?

- Turnaround clarity: are timelines explained realistically, including validation and publication timing?

- Support access: is there phone and email help when a structure is not straightforward?

- Renewal options: are there multi-year choices and reminders to reduce annual admin work?

- Data maintenance: can legal name, address, or status changes be updated without extra friction?

- Pricing transparency: are fees clearly posted, with no uncertainty around what is included?

For Canadian entities that want a straightforward route, LEI Service positions itself as a registration agent for a GLEIF-accredited path and offers new registrations, renewals, transfers, multi-year management, and support by phone and email. Its published model is clearly geared toward speed and ease of use, with same-day processing in some cases, express handling, duplicate-prevention checks, and free updates to keep reference data current. That kind of support can be especially useful when a fund team is working against a launch deadline or a renewal date.

Renewal and data updates for an investment fund LEI

An LEI is not permanent in an operational sense, even though the identifier itself remains tied to the entity. The record must stay current.

Annual renewal is the part most teams remember. Event-driven updates are often the part that gets missed. If a fund changes its legal name, registered office, legal form, status, or ownership information, the LEI data should be updated promptly.

A lapsed LEI can be nearly as inconvenient as having no LEI at all. Counterparties may flag it. Onboarding teams may pause. Reporting processes may become messier than they need to be.

The easiest way to keep control is to treat LEI management as part of entity governance, not as an isolated admin task.

That usually means:

- calendar reminders well ahead of the renewal date

- a central inventory of every entity and its LEI status

- a compliance review whenever the fund undergoes a legal change

- one named owner internally, even if the work is outsourced

Why fund groups should centralize LEI oversight

This is where many organizations can make a quick operational gain.

If a fund sponsor has several vehicles, renewals and updates are much easier when managed from one central register. That register can track the fund, feeder, master, GP, manager, and any parallel vehicles together with issue dates, renewal dates, and supporting records.

Without that central view, teams often find themselves chasing the same information more than once, or worse, renewing one entity while missing another that is about to trade.

Practical timing for Canadian investment funds

Canadian funds often face a mix of local and cross-border requirements. A strategy marketed or traded outside Canada can bring in external reporting and counterparty expectations quickly. That is why the best time to arrange an LEI is usually before the first regulated activity, not after the first urgent email from a broker.

Simple entities may receive an LEI quickly. Complex fund structures may take longer, especially if validation depends on extra documentation or less familiar formation records.

The practical message is clear: if a fund expects to trade, use derivatives, onboard with institutional counterparties, or enter a reporting chain, the LEI should move onto the launch checklist early.

For teams that want a faster path, a provider with strong support, clear pricing, and active data maintenance can remove much of the friction. In Canada, that is often the difference between a routine setup task and a last-minute delay no one wanted.