Express LEI Issuance: When You Actually Need It (and When You Don’t)

Speed sounds reassuring when a trade, filing, or onboarding request is already on the clock. That is why express LEI issuance gets attention. If a legal entity suddenly needs a Legal Entity Identifier to execute a transaction or satisfy a compliance check, waiting even one business day can feel too long.

Still, “urgent” and “necessary” are not always the same thing. In many cases, standard LEI processing is perfectly adequate. According to GLEIF, there is no required global service-level timeframe for LEI issuance, though most LEIs are issued within 24 hours. That makes express service valuable in the right moment, but not automatically the smart choice every time.

What express LEI issuance actually means

An LEI is a unique identifier for a legal entity, not a natural person. A corporation, fund, charity, trust structure, or other organisation may qualify. An individual acting personally does not receive an LEI. That distinction matters because many last-minute requests start with confusion about who the identifier is for.

Express issuance usually means a registration agent or issuing organisation prioritises validation, document review, and submission so the LEI can be published faster. It does not mean the checks disappear. The LEI still connects to verified reference data drawn from authoritative local sources, and each LEI can represent only one entity. Good speed depends on clean entity data, prompt review, and efficient handling, not shortcuts.

There is another practical point that often gets missed. The public LEI record is updated daily. So the true question is not just “How fast can an application be filed?” but “How quickly can the validated LEI appear in the public index so a counterparty, venue, or bank can see it?”

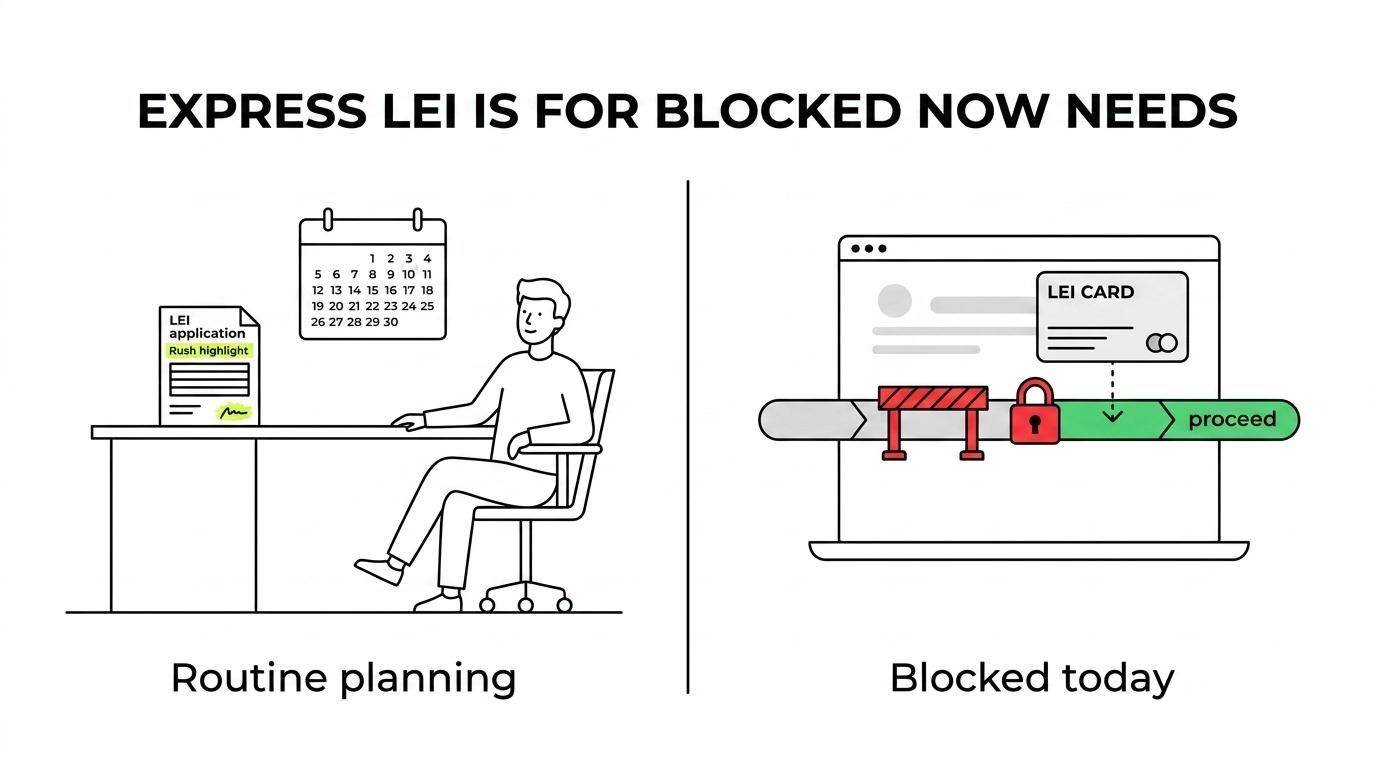

When express LEI issuance is genuinely necessary

Express service makes sense when a transaction or reporting obligation is blocked without an active LEI. This comes up often with market access. A broker or trading venue may refuse to proceed until the legal entity’s LEI is visible and active. For a business with a trade window, a funding event, or a regulatory deadline that cannot move, speed stops being a luxury.

It also matters for Canadian entities dealing outside Canada. Under MiFIR, EU investment firms must identify legal-person clients with LEIs for MiFID II transaction reporting. Trading venues also need issuer LEIs in daily submissions to FIRDS. In the United States, CFTC rules require each counterparty to a swap under its jurisdiction to be identified by a single LEI in recordkeeping and swap data reporting. If a Canadian legal entity is entering that kind of transaction, the requirement can arrive through the market or counterparty even if the entity itself is not based in Europe or the U.S.

A common mistake is assuming regulators will grant extra time. ESMA did allow a temporary six-month grace period when MiFIR took effect on 3 January 2018, but that was a launch-era accommodation, not an ongoing safety net. Today, firms should act as if the LEI is needed before trading starts.

When express issuance is worth paying for, the trigger is usually one of these situations:

- Trade deadline: a bank, broker, or venue will not execute until the LEI is active

- Regulatory reporting: a transaction must be reported with the entity properly identified

- Entity onboarding: a new relationship is being opened for securities, derivatives, or treasury activity

- Lapsed status: the LEI exists but renewal has been missed and a counterparty wants it updated now

When standard LEI issuance is usually enough

If the entity is planning ahead, standard processing is often the sensible option. Most LEIs are issued within 24 hours, which is already fast enough for many internal compliance projects, account opening processes, and pre-trade preparation. Paying a premium for express treatment only makes sense if timing is genuinely tight.

Annual renewal is another example. LEIs are renewed every year. If the expiry date is still weeks away, there is little value in rushing. Multi-year management can reduce the risk of last-minute renewal pressure, especially for entities that trade regularly or have several teams relying on the same LEI data.

This is where a bit of discipline saves money. If the legal department, treasury team, fund administrator, or compliance function knows an LEI will be needed, ordering it early gives everyone more room to correct any data mismatch before it becomes urgent.

Standard timing is usually enough in situations like these:

- routine renewal well before the anniversary date

- account setup with a generous lead time

- internal compliance preparation

- planned fund or issuer onboarding

- low-pressure vendor or bank documentation

A practical table for deciding on express LEI issuance

The easiest way to assess urgency is to match the business event to the real deadline. If the LEI is a gatekeeper to an action happening today, express service is often justified. If the LEI is part of a process scheduled next week or next month, standard service may be perfectly fine.

| Situation | Express LEI issuance? | Why |

|---|---|---|

| A trade cannot be placed without an active LEI | Yes | Market access may be blocked immediately |

| A swap counterparty needs the LEI for reporting now | Yes | Reporting and recordkeeping obligations are time-sensitive |

| A fund or company is opening accounts for launch next month | Usually no | Standard processing should fit the timeline |

| Annual renewal is due today and a bank checks active status | Yes | A lapsed LEI can interrupt transactions or onboarding |

| Annual renewal is due in three weeks | No | Standard renewal is normally sufficient |

| An individual trader wants an LEI personally | No | LEIs are for legal entities, not natural persons |

| A corporation is preparing for possible EU trading later this quarter | Usually no | Early standard issuance avoids unnecessary rush fees |

What affects LEI issuance speed for Canadian legal entities

Fast issuance depends heavily on data quality. If the entity’s legal name, registration number, address, and jurisdiction match the official registry record, validation is straightforward. If they do not, delays become much more likely. Even a small mismatch in punctuation, legal suffix, or registered office details can slow things down when the application has to be checked manually.

Duplicate prevention is part of this as well. A reliable registration process should look up existing records to avoid assigning a second LEI to the same entity. Since every LEI is unique and tied to one entity only, duplicate controls are not optional. They protect the integrity of the Global LEI Index and save applicants from a much bigger administrative problem later.

When timing is tight, these details matter most:

- Exact legal name: match the registry record, not the brand name

- Entity status: active legal entities are easier to verify than entities with unresolved registry issues

- Authorised requester: the person placing the order should be able to act for the entity

- Accurate registration data: numbers, addresses, and jurisdiction details should be current

One more point deserves attention. Speed claims should be read carefully. Since GLEIF does not impose a universal issuance deadline, providers can only speak to their own handling times. A promise of “express” has value when the provider also explains its cutoff time, document expectations, and what happens if the registry record needs manual review.

Express LEI issuance versus express LEI renewal

A new LEI request and an urgent renewal are not quite the same thing. New issuance requires the entity to be identified and entered into the system. Renewal updates the existing LEI reference data and confirms it remains current. If a legal entity already has an LEI but its status is no longer current, express renewal can be just as important as express issuance because many counterparties care about active, up-to-date status rather than the mere existence of a code.

For businesses that trade regularly, renewal pressure often causes more disruption than first-time registration. That is why proactive annual management matters. Some registration agents offer multi-year plans, same-day processing if the order arrives before a morning cutoff, and even two-hour express service. Those options can be useful, though the stronger strategy is simple: renew before the deadline and keep the reference data current throughout the year.

How to choose an LEI provider when time is short

When urgency is real, support quality matters almost as much as speed. LEI issuers and registration agents are the primary interface for legal entities seeking an LEI, so responsiveness can shape the entire experience. If questions about entity type, documentation, or registry details are answered quickly, the application moves. If support is slow or unclear, “express” becomes a label rather than a result.

A sensible provider choice rests on a few operational basics. Clear pricing helps. So do included GLEIF fees, duplicate checks, and free updates to reference data where available. Phone and email support can make a major difference when a filing cutoff is close or when a corporate structure needs clarification.

Useful signs to look for include:

- transparent processing cutoffs

- express options with stated turnaround times

- registry and GLEIF lookup before submission

- support by phone and email

- simple renewal and transfer handling

Express LEI issuance for Canadian entities active in foreign markets

Canadian organisations often meet LEI requirements through cross-border activity rather than domestic habit. A pension-related vehicle, investment fund, treasury entity, issuer, or corporate group may only realise the need when dealing with an EU investment firm, an international broker, or a derivatives counterparty. In those cases, the requirement can appear suddenly, even though the rule itself is longstanding.

That is why the best time to ask about an LEI is before the first blocked trade, not after. Any legal entity entering into a financial transaction may be eligible for an LEI, while the legal requirement to hold one comes from the relevant regulator or market rule. A quick internal check with the broker, venue, bank, or legal team can often confirm whether the entity needs an LEI now, soon, or not at all.

There is also a useful reality check here. If the applicant is a person acting in an individual capacity, an LEI is not the answer. If the applicant is a legal entity and a financial counterparty is asking for the identifier, the request should be treated seriously and early.

The simplest way to decide

A good rule works well: pay for express LEI issuance when the absence of an active LEI will stop revenue, trading, reporting, or onboarding today. Use standard processing when the need is known in advance and the timeline still has breathing room.

That approach keeps urgency focused where it belongs. It also protects budgets, reduces compliance stress, and gives legal entities a cleaner path into the markets where the LEI is already part of the entry ticket.